Advisor Resources

Insights to help grow your business and improve your clients' financial lives.

Go to topic

Featured

Most Recent Posts

-

Betterment for Advisors Case Study Q&A: How Ritholtz reaches a new client segment

Betterment for Advisors Case Study Q&A: How Ritholtz reaches a new client segment Matt Lohrius oversees the Liftoff platform at Ritholtz Wealth Management, which began leveraging Betterment’s platform more recently. Ritholtz is located in New York City and manages more than $2.7 billion in assets. Non-paid client of Betterment. Views may not be representative, see more reviews at the App Store and Google Play Store. Dan: Tell us about how the sort of robo-advisor aspect of things works within Ritholtz Liftoff. How do you guys organize it and think about it? Matt: As you probably know, our core business was focused on high net worth households, people that were staring down retirement or leading up to it. And we put out a lot of content—whether it's blogs or The Compound (our YouTube channel)—so a lot of people are following us and telling us they’d like to become clients. But many of them didn’t fit our traditional high net worth, pre-retirement customer profile. But clearly there was a demand, and we wanted to help these people. So that's why we created Liftoff, which we’ve continued to improve over the years. But it really blossomed once we started working with automated platforms like Betterment. There’s no minimum, so it’s great for people in their twenties or thirties who are maybe just starting to invest. Dan: Tell us a little bit more about Liftoff’s ideal client profile. Matt: There are a couple of different types. One would be someone who's on the younger side and who is in the accumulation stage base. They may not yet be married or have a family, but they’re starting to make money and they want to save in a smart way. This type of investor also wants access to an advisor for questions that do arise: around what they should be doing differently when they do get married or start having kids. I also love talking to people who have just graduated college, because they’re such enthusiastic followers of ours. We’re happy to accommodate them. Dan: This is obviously a big potential for growth. How do you think about growing Liftoff? Matt: I think we want to grow it as big as we possibly can and take it as far as we can. And that's kind of my mindset: I get on the phone with everyone who wants to chat. Hopefully we do get to the point where we need to bring more of me to oversee twice or three times as many Liftoff clients as we have right now. Dan: What have been the biggest hurdles to growth so far? Matt: One hurdle is that there's always going to be people out there that would rather just do it themselves and that's fine. We totally understand that. But there are still plenty of other people out there who don't even know where to start. And so we're looking to reach that group of people. Dan: Do you find that there is a catalyst that brings the self-directed types to you? Matt: Yeah, it could be a year like this one that we're in right now where people who have been investing on their own for a while reach out because of all the uncertainty. They are looking to get a little more advice. Dan: Talk a bit about the culture within Ritholtz to new technologies. Matt: We're all about it. Outside of the Liftoff channel, Ritholtz is looking at technology to onboard clients more quickly and smoothly. We know it’s possible—with Betterment and Liftoff, you can open an account like that. So we want to be able to expand that kind of capability throughout our entire firm. And that really just involves us looking at all the technology we currently have to streamline the client experience. Dan: Can you talk a little bit about the difference that an automated platform like Betterment makes in your day? Matt: For Liftoff, it’s just huge from a technology standpoint: opening accounts, transferring money from other custodians, depositing money, linking a bank account. Everything is so easy and intuitive for the client. And that saves us a lot of time: we’re not having to help a client with the logistics of opening an account and can spend our time with them focusing on advice. That's where platforms like Betterment really excel, with the operational efficiencies. I think a lot of advisors hear “robo-advisor” and sometimes get a little turned off, but who doesn't want operational efficiency? And that’s on both sides of the equation to clients and advisors. Dan: What if you go back, what initially sparked the interest in convincing you to start using a robo-advisor as a partner? Matt: It’s kind of just set it and forget it. It's easy. You have a durable, long-term portfolio. You're going to invest in it just to keep saving. That's the work that you need to do, is constantly save. And outside of that, you don't need to do a whole lot. It's helpful for a lot of people. And when we do have a client ask “Can I do my own thing?"—because there’s often that temptation—we tell them “No, you can't.” That's the whole purpose and benefit of this. You can go somewhere else and do that. But if you want a concrete long-term plan, this is where you're going to get it, and it's very likely to work. Dan: What would you tell advisors who are skeptical about using a robo-advisor? How would you help them to understand how well it's worked for you and your clients? Matt: People who are skeptical need to realize that this is a hybrid platform. Yes, the portfolios and operations are automated, but you have access to an entire firm. Because if you have access to me, you have access to all the resources that I have access to. And that can be powerful. Dan: Last question. Does using an automated platform like Betterment mean that you, as a CFP®, as an advisor, get to spend more time on bigger issue questions like planning? Matt: Yes, one hundred percent. That is the whole reason Liftoff switched to Betterment. With the custodians we had been using previously, there were a lot more operational emergencies that needed our time and attention. But with a platform like Betterment, all of that is taken care of so that we at Liftoff can focus solely on providing quality advice. That's all we want to do here. Automation (through Betterment’s platform) is allowing us to do that now, which is why I'm confident that Liftoff will continue to grow. Ritholtz Wealth Management is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where Ritholtz Wealth Management and its representatives are properly licensed or exempt from licensure. This website is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by Ritholtz Wealth Management unless a client service agreement is in place.

-

Q&A with Paul Sydlansky of Lake Road Advisors

Q&A with Paul Sydlansky of Lake Road Advisors A conversation about going independent and scaling your business using the Betterment for Advisors platform. Paul Sydlansky is the founder of Lake Road Advisors, an independent, fee-only financial planning firm. He has worked in the financial services industry for over 20 years. Prior to founding his firm, Paul worked as a relationship manager for another RIA. He also spent 13 years at Morgan Stanley in New York where he was a senior level manager in the institutional equities department. Paul is a Certified Financial PlannerTM, a member of NAPFA and a member of the XY Planning Network. Non-paid client of Betterment. Views may not be representative, see more reviews at the App Store and Google Play Store. Q: Tell us a little bit about your practice and the factors that you think have contributed to your success in growing your RIA. Lake Road Advisors is an independent, fee-only financial planning firm. We specialize in working with mid-career professionals who have young families and that's been developing over time as our niche. Right now we have about 100 client relationships and manage roughly $60 million in assets. We have offices in upstate New York and in Long Island. We launched the firm in 2016. Before that, I was at a RIA where my views, goals, and values were not in line with the firm owners. For me, launching the firm was about sticking to my views – simplifying things for people, making things easy, and really focusing on what adds value to my clients. And for the niche that I work with, it's having somebody who is an accountability partner – somebody to bounce ideas off of, who can worry about all these things that generally folks don't have time to do, but they realize are super important. Focusing on those clients’ needs and making their lives easier has really led to our growth. Q: What were the biggest hurdles that you encountered when you were initially growing your practice, and how did you navigate those? Starting from scratch. I had a non-compete at the firm I left in 2016 so I had to start with nothing. Planning out my runway was difficult. I think for anybody who's thinking about starting their own firm, it's always going to be longer than you assume – if you're budgeting, I recommend you assume the worst and then add two or three times that in terms of how much you need. That was very difficult for me, starting from a position where really all you had to focus on for the first year or two was growth and making sure that I was developing enough of a client base to make the business viable. I was lucky that we had some good growth to start with and now my challenges are all different. But that was the biggest one – making sure that financially I had enough runway, I could still live the life I wanted and support my family while I was doing it, and making sure I was doing things the right way. Q: What role has Betterment for Advisors played in your growth over the last few years? When I was at Morgan Stanley, I was in private wealth management for a couple of years, but I spent the majority of my time in prime brokerage working with hedge funds. So I came into the financial planning business with a kind of skewed view of investments. I'll be honest, I believe in hedge funds and alpha creation and the ability to outperform. And as I've evolved as an advisor, I've really done a 180 and realized that for the majority of people, trying to chase alpha is not really going to change their life. What's going to change their life is focusing on blocking and tackling their cash flow, their spending habits, their balance sheet, not making silly decisions, creating good habits. Of course, we'd all like extra return. But I think the pursuit of that is going to be fruitless for most, and for the majority of people, having a simple, low cost, diversified portfolio just makes sense. So the firm I was at was an active manager and I saw firsthand what a disaster that was, to try to manage 800 individual portfolios and do things like tax-loss harvesting or rebalancing. It was just a nightmare and they spent a ton of time doing it. And in my opinion, it didn't really add much value to the end user because the manager was actually underperforming a lot. So for me, Betterment was number one given that the platform is easy to explain to my clients. Most of my clients obviously understand investing, but they don't want to spend too much time on it. Betterment allows me to do that. It's straightforward. They have one page in the app where they can click to see their performance and really quickly understand. It keeps things super simple. I don't spend any time on things like rebalancing, I don't spend any time on things like tax loss harvesting. It's all automated. And I know that frees me up to do things that actually will add value to clients. Q: Is all of your AUM at Betterment or do you use other custodians as well? Yes, so the majority is – I have a portion of it that is with Vestwell on their 401(k) platform. I have no other partners – it's all Betterment for my individual clients and then for my five clients who are on the 401(k) platform as well, that's the other system I'm using. Q: How does Lake Road position Betterment for Advisors to its clients? I've obviously had this conversation tons with different advisors. Everybody seems to be hesitant to partner with Betterment, saying – well, aren't they your competitor? Absolutely not. Because the way I view it is Betterment is a partner and a technology platform. So that's how I position it. First and foremost I say I'm a registered investment advisor. I am not a bank, I am not a broker-dealer. I've partnered with another firm who can allow me to leverage a system that really buys in perfectly to how I believe investing should be done for almost everybody. So for me, I position Betterment as a partner, as a technology solution, and I don't see it as competition. Q: How do you price your offering and how do you communicate your firm's pricing to your clients? Great question. What I do is tell the client one all-in price because as everybody knows, pricing can be confusing, and I try to just be as straightforward as possible. For anybody under a million in AUM, it's 1.25%. And again, usually it's a half a million minimum of assets. And the way I tell that to clients is that ultimately, I have a set amount that I'm trying to make for the firm, and a percentage does go to me, and a percentage goes to Betterment. My fee is for the planning work and obviously helping with the investments. And then part of that fee goes to Betterment for the technology and for all the tools that they're providing us to use. But I like to present it as an all in fee. And in addition, I have breakpoints. So if a client hits a million, that all-in fee drops to 1.1%, and then so on. I also have another offering where I have clients who have no investment management. It's just straight planning. And for those clients, it's a flat $5,000 a year. They are not on the Betterment platform, but it's another way for me to work with young families or folks who have assets tied up in their business and don't have the assets to manage right now at this point in their life. I'm up front with clients and say, “I only have so many seats on my bus.” I have one other gentleman who started working with me late last year. And so now that we have 75 relationships, ultimately I'm looking to try to make $5,000 minimum on each one of those seats because I know the amount of planning work we do. I know how many touch points we have, how many meetings, how many calls, how many zooms, how many visits. And so for me, that's kind of the minimum where I want to be with the amount of service that we're going to provide, the relationships that we're looking for to grow the business. Q: Are you typically using Betterment’s investment portfolio? Are you using different portfolio strategies for clients? Right now I'm using Betterment strategies for the majority of clients. I thought about creating my own portfolios but for the amount of time it would take me to research and keep on top of it, it just didn't seem like I was adding any value there. In addition to the Betterment portfolios, I've used the BlackRock portfolio, one of the income generating portfolios for a client where it was appropriate. Q: Aside from Betterment for Advisors, what else is in your tech stack? I use MoneyGuidePro on the planning side and my CRM is Wealthbox. I've been using Riskalyze and I've been really happy with them in terms of storing and having an IPS, and it's a great conversation starter and just a way to explain risk a little bit better to clients. I use Calendly. I think most people probably use something, but Calendly has been a huge time saver for me, for my business. Q: What are your client acquisition strategies? I've been pretty lucky in that when I look at the tracking of where my clients have come from, they've been pretty evenly split from a lot of different sources. The first has been friends and family. Another one is current client referrals. And a third one has been networks or traditional centers of influence like lawyers and accountants. In terms of marketing, I write a blog. I have over 100 blog posts now and while it was tough to do, it's a really good marketing tool. I answer questions on it that I hear all the time from clients and prospects. So if a client or a prospect reaches out I can tell them I just wrote a blog post about that. I also started to do some videos. Creating awareness and really connecting to your niche or your target market is huge. I went through the exercise of figuring out exactly who I want to work with and with everything I do from a marketing perspective, I try to speak to that person. That’s really been a driver of growth. Q: What would you tell advisors who might be skeptical of using a platform like Betterment or something similar? You need to think about your practice and where you add value to your clients. I do believe that there are folks out there for whom active management can make sense in some instances. But I think you really need to figure out how you're positioning your firm for the future – is it the planning you're going to focus on or is it the investment management? Where are you going to add value? What's going to differentiate you from other advisors? If you think that you're going to be focusing on planning and the relationship and accountability and all that type of stuff, choose something that automates other work for you. Because you going in and clicking a button to rebalance does not add any value and it just takes away from other things you could be doing. Q: How do you answer questions from clients that want to have positions that aren't part of the Betterment models, such as single stocks? What do you tend to say to them? Yeah, that's a great question. So I think that goes to fit upfront. I have a conversation upfront about my investment philosophy and how I don't really believe in holding individual positions. Ultimately, we do work with some executives and they have restricted stock and individual positions and options and you can't get around that. So what I tell people is if you're going to have individual stocks, by all means have a Fidelity account. Have a Charles Schwab account. Have a Vanguard account where you can do that as long as you want to trade it on your own and you're doing it outside of what you’re doing with me. Q: As an advisor who's also a business owner, how do you keep up with compliance as you grow your business? When I launched my firm, I launched with XY Planning. They helped me get up and running, but I outgrew it and needed a little bit more help. Since I'm in New York, I had to be SEC registered. I work with an individual who basically opened up a compliance firm that helps folks like us – the smaller size advisor. So I have an individual lawyer who helps me with the compliance. Because I'm still on the XYPN platform, I also use something called Smart RIA that's like a CRM for all of your tasks and all the things you have to do for compliance. And the other thing is, my business is super simple because of the nature of the investing. For anybody who's done the ADV, a lot of the questions are around investing and advice and things like that. My investments are so simple and so vanilla that I think because of the reduced complexity, it makes compliance a little bit easier. Q: Do you have any advice on how to coordinate your IPS with the Betterment portfolios? As part of my onboarding process, I make people go through the risk process. I use Riskalyze which connects with Wealthbox. So I check a box, and once a risk score is in Riskalyze it flows to Wealthbox, and it populates a field for me so I can see the score when I pull up the client. And then on top of that, when we start building out their plan in MoneyGuidePro, we have the ability to make sure that that score translates to Money Guide Pro. It’s not perfect right now, but it goes between those different systems. Q: The transition to remote work has been a popular topic. How have you adapted to that? Is there anything new or different that you're doing to connect with clients and prospects? No, remote work has honestly been completely seamless. From a system standpoint, I worked from a home office already. From a marketing perspective, it's really made me realize how important your online presence is. Everybody knows your website and blog and all that is important, but I started doing video too because I feel like it's a better way to connect with people. I've been using something called Loom, and I also took a class about how to do videos and best practices. Before I meet a prospect, if somebody reaches out online, I will send them a quick 20-30 second Loom video saying: Hi, I'm Paul. Thank you so much. I'm really excited to meet you, if you could just prepare this and that for our meeting, and so on. I've been told it has been really positive because people feel like they know you before they talk to you. Now I'm trying to incorporate it into my client service process too. So every once in a while if I have a follow up task, I can send someone a quick video and say, hey, it's Paul, we took care of that Roth conversion, you're all good to go, have a great day. Little things like that, I think those are going to be more important going forward. Seeing people on Zoom can be tiring, but getting a quick short video from somebody, a friend or somebody who's helping me with something, it's really nice versus an email. So I do think for me and my firm, it's going to be more focused on video, leveraging that and using that as a way to connect. Q: One last closing question: What advice would you give to new advisors who are just starting out? Aside from making sure that you have enough cash to weather the storm of the ups and downs, I think the other thing is making sure if you have a spouse or partner, whoever's going to be there with you, that they're bought in. Aside from the financial stress of starting something new, don't discount the emotional ups and downs you go through on a day to day basis. Having somebody who's supportive and who can be there in the good and the bad is very important. Your emotions go all over the place and it's still that way. As an owner, I don't know if it will ever change. I think it's leveled out a little bit but I still want to grow. If you would have told me when I started where I’m at now, I'd probably be really happy. But now I want to get to $100mm or $250mm. I'm thinking about my firm and what people I need to help me get there. So I just think having support at home from that person and making sure they're bought in is huge. Because if you don't have that, it's probably going to be difficult to do it.

-

Advisor Spotlight: Katelyn Bombardiere, Commas

Advisor Spotlight: Katelyn Bombardiere, Commas For this Advisor Spotlight, we welcome Katelyn Bombardiere, CFP®, a Financial Planner at Commas, to chat about her passion for helping the everyday investor. Non-paid client of Betterment. Views may not be representative, see more reviews at the App Store and Google Play Store. Advisor: Katelyn Bombardiere Firm: Commas Bio: Katelyn Bombardiere, CFP®, is a Financial Planner at Commas, a fee-only financial planning firm based in Cincinnati. Katelyn started her career in the high-net-worth wealth management industry where she quickly realized her passion for helping the "everyday" investor. She sought a different approach to help people (like her friends, family and peers) without worrying about asset minimums. Firm Bio: We all don't have millions of dollars—but we all have goals. Commas is a financial advisory that provides fee-only service to the EveryInvestor: those who might not fit the standards set by traditional high-net-worth advisories but still deserve personalized financial guidance to meet their goals. We offer services with no account minimums, working with our clients at every step of the process and empowering them to create, plan, and achieve their desired money goals. We Are: Encouraging: 0% Judgment Trustworthy: Certified, Not Stuffy Purposeful: Fee-only for All Approachable: We Wear Jeans Why did you decide to become an advisor? As a sophomore in college, I was fortunate enough to go on a trip through the Leeds School of Business at The University of Colorado at Boulder. This trip took a group of students to over 10 different financial firms to introduce them to the possibilities of careers in finance. It was on this trip that I declared my major as finance and figured out that I wanted to be a wealth advisor. From there, I pivoted my internship and career choices to pursue my goal of becoming an advisor. What are some questions that you wish more clients would ask, and why? I think it is important for people who are looking for an advisor to know: if the advisor they are talking to is a fiduciary how that advisor is getting paid the investment philosophy and financial planning process the advisor follows what the advisor's qualifications are. I think gauging a sense of the advisor's passion is important too. You want to work with someone who is passionate about what they do, continues to learn, and shows an interest in you. What do you think is the biggest mistake people make with their money? Either they don't save enough, or they save but don't invest. Another big mistake is not understanding the difference between long-term investing in well-diversified funds and day trading. What does your firm's current tech stack look like? How has technology impacted your work? We utilize Betterment for Advisors as our custodian and Right Capital as our financial planning software. We have created our own CRM platform using Airtable which is a zero code cloud spreadsheet database. This tool allows us to customize our own portal where we house client data, tasks, meeting notes, and the client ledger (types of accounts, where they are held, contributions, notes, etc.). What makes Commas unique, however, is our internal automations through Zapier. For example, after our introduction meeting, the prospect is automatically sent an email with the next steps (signing up for our fee, completing a questionnaire and opening a Betterment account with our client agreements). Once they complete that step they are automatically sent another email asking them to upload documents to our secure portal. Those documents then file themselves into the correct client folder. The clients are then prompted to schedule our discovery meeting. This process continues all the way through the client onboarding process, and even when it comes time for generating annual reviews. These automations are what allows us to service our clients more successfully. They decrease the time we spend on busy work—account opening paperwork, filing documents, creating review outlines, sending template emails, etc.—and increase the amount of time we get to meet with clients and work on their financial plans. How have the recent trends toward remote and hybrid work impacted your relationship with clients? The remote work trend has only strengthened our client relationships as we were already well equipped from a technology standpoint. Our client meetings are generally 30 minutes to an hour, which is on the shorter side when looking at some other wealth management firms. I think our clients like the ability to have a quick meeting and get back to their day. They are just as busy as we are! This also allows us to work with clients all across the country. What do you think is the biggest opportunity for advisors today? To work with the everyday investors and show them that they are qualified to work with an advisor. You don't have to have thousands or millions of dollars to get good financial advice from a trustworthy source. This is also an opportunity to prove that fiduciary financial advisors are trustworthy professionals, not shifty sales people. If you won the lottery, what would you do with the money? Treat myself to a nice international vacation, set aside some funds for my closest friends and family (as long as they invest it for their futures), and invest the rest to ensure that I can attain all of my goals and retire comfortably. If you could only give one piece of financial advice, what would it be? If you are young, start investing today—even if it is $10/month! If you are older, still get started today! I also can't help but advise that you talk to a financial advisor (fiduciary!). Every single person's financial situation is different, and having the peace of mind that you are on track is so powerful. Yes, you can absolutely do this on your own, but do you have the time or passion to do it? Will you be 100% confident in your choices? If you are sick, you go to the doctor. If you have a toothache, you go to the dentist. If you have finances to manage (spoiler alert we all do), why not talk to a financial advisor?

Explore our expert commentary

Expert Insights

-

![]()

Betterment for Advisors Case Study Q&A: How Truepoint lowered the cost of serving more clients

Betterment for Advisors Case Study Q&A: How Truepoint lowered the cost of serving more clients Founded in 1990, Truepoint Wealth Counsel is an independent and nationally-recognized RIA based in Cincinnati, managing over $4BN in AUM and voted among the 2020 Top Workplaces by the Cincinnati Enquirer. Non-paid client of Betterment. Views may not be representative, see more reviews at the App Store and Google Play Store. Betterment’s Alex Choi recently sat down with Brad Felix, portfolio manager at Commas (formerly RhineVest), a subsidiary of Truepoint Wealth Counsel, to hear about how the firm has successfully leveraged the Betterment platform to grow the practice. Alex: Tell us a little bit about your practice and the factors that have contributed to your success. Brad: When Commas started in 2015, I realized how technology was changing the wealth management industry. Betterment was one of the disruptors driving that change, and we saw how the Betterment for Advisors (B4A) platform could lower an advisor’s operating costs. We wanted to leverage those cost savings to serve those who don’t necessarily have a million dollars (and that’s a lot of people). We've grown from 0 to 338 households since 2015. Growth was supercharged when Truepoint Wealth Counsel acquired our firm in 2016 and there’s been no looking back. Alex: How does Truepoint think about segmentation and where does Commas fit in? Brad: Today, Truepoint’s True Wealth service offering represents our firm’s bread and butter where we provide tax and estate services. But we still want to serve other clients well and do right by them. So segmentation just makes sense, and the Commas/B4A combination offers a great solution. B4A and Commas started by serving clients with less than $1 million but are now starting to serve clients in the $1 to $3 million tier as well. Alex: What were some of the biggest hurdles you encountered while you were initially growing your business and how did you navigate those? Brad: I think the hardest thing for every new firm is distribution; and with the less than $1 million client segment, it can be a challenge to convince people that they need a financial planner. A lot of people feel like they don't qualify. So the first marketing push was letting people know that they had options beyond an insurance company or a bank, and that fee-only fiduciary advice was available regardless of how much money you have in your investment accounts. We tried to do that in a number of ways: a kind of radical, very transparent website that clearly showed pricing and the fact that we had no minimums. We created an edgy brand to show that we don't take ourselves too seriously and that everyone needs and deserves access to financial advice. We've also done some work around search engine optimization (SEO), focusing on keywords like “financial planner” and local searches in our Cincinnati geographic area. We like to rank well in those local searches and believe that our memorable brand and website helps us attract new clients. I think there's an advantage to being different when compared to lots of financial planners that kind of look the same. I would encourage others to define a unique message and lead with that because it does help you stand out. Although things were slow at first, at some point it just clicked. Delivering on your promises and serving clients well will get that flywheel going where they're telling their friends about the good experience they've had at your firm. Alex: I have always been a big fan of your firm’s website. Can you talk a little more about your process for building that out and why you chose to include what you did? I think a lot of our clients aspire to build similar type sites and would appreciate how you went about it. Brad: I appreciate that. We worked with a really good local designer who pushed us to come up with a very simple message about why we were unique, why we were different. Our biggest goal for building out our site was transparency. We know that consumers are tired of landing on websites and still not being able to understand how much they would pay for something. We’re very clear, very upfront because in our minds this is the first stage of trust. We want people to talk to us, so our “let's talk''' button is all over our website. If the website conveys enough trust to get them to have a conversation, then we can be successful in moving them to the next stage to be a client. We felt that Betterment had an attractive product so any chance we had to note our decision to utilize Betterment’s B4A offering and also to highlight how we're providing value to the client seemed to resonate with people. Alex: So how does Commas position Betterment for Advisors to its clients? Brad: We describe Betterment as our technology partner. Given Betterment’s increasing brand awareness, we talk about Betterment alongside Fidelity and Schwab, and people are comfortable. It’s part of our tech stack just like anything else. In addition, we're in the business of financial planning. It's what we do. In that vein, we've always viewed Betterment as a complementary partner, not a competitor. Alex: How do you price your offering, and how do you communicate your firm's pricing to clients? Brad: Our financial planning fee is $65 a month, but we also believe investment management is an essential part of the whole package. Our investment management fee is 80 basis points, which includes the Betterment fee. Alex: Does Commas leverage some of the client behavior functionality like goals-based planning modules and behavioral guardrails? Brad: Well, to be honest, the advantage of partnering with Betterment is that it also has a retail product and you put in the research to know what's a good feature, what's a good design choice, how do you get a better outcome, better behavior, etc. We honestly try not to interfere with the work you all do there and really just let the platform guide our clients and focus them on what we do best. We really spend most of our time on financial planning and just working through all the goals a client has set up in the Betterment system. Alex: Can you tell me some ways your practice has become more efficient? Brad: Very simply, the Betterment platform significantly lowers our cost of doing business. So account sign up, trading, cash management, those are all ways that we're not spending money on labor. We’re maybe unique among the firms that are using your platform in that we never intended to use Betterment as a solution only for children of our clients, but we now find that we can serve as many people as possible. Automation and efficiency are key to our profitability, because we provide great service at a higher client to advisor ratio vs. the industry. Alex: Could you just kind of take us through what the experience would be for a new client from when they hit your website to you guys actually opening and transferring their assets and where Betterment may fit into an onboarding workflow? Brad: The Betterment technology helps us to compress our onboarding cycle considerably, sometimes to as little as a day. At the end of an introductory client meeting, we send a welcome email that has a link to the questionnaire that helps us learn more about them, a link to open a Betterment account, and a link for our financial planning fee. The client signs our agreement as part of the automated Betterment signup process. Depending on what they fill out in the questionnaire, there may be additional automated follow-up. For instance, if they have certain held away assets, another email asks for more information. Once all the information is received, the advisor can then get a good look at their entire financial picture so that at the first financial planning meeting the conversation can focus on what's important to the client, rather than all the administrative details. Alex: What additional tools and automation do you employ along with Betterment? Brad: We subscribe to the “low code” or “no code” technology trend. The whole idea is that you don't have to be a developer to create automation between different systems. And that's really the whole premise of what we started experimenting with three or four years ago. We started using Zapier to tie together different pieces of our software. We use Typeform for our initial client questionnaire that we send out and that questionnaire is delivered by Mailchimp, which is a common email service. We also had a CRM at the time, so linking all those together. The basic discovery workflow started when a client booked a meeting through Calendly and then received the questionnaire. Ultimately that information would flow back into our CRM without our advisors doing anything. We were focused on determining how we can spend more time talking with clients and thinking critically while automating everything where human interaction doesn't add value. Alex: So it sounds like you’ve compiled a pretty big tech stack. Do you still find from a unit economics perspective that all those monthly subscriptions are saving you money? Brad: Yes. Our tech stack is not your typical financial industry tech stack. We're bucking the trend on what people say we should use and looking at other industries to find different, innovative tools. We’ve found that pricing for these non-industry tools is dramatically lower. We got rid of our CRM and now use Airtable, which I think everyone should check out. We use a client-to-advisor ratio to help us guide profitability. In a standard firm, this ratio is roughly 100 to 1. Even at 200 to 1, we would have profitable outcomes, but at 300 to 1, we’d feel really confident that creating business in this segment can deliver industry-like margins. It's just a different type of model. It's higher volume, perhaps less complexity, but requires a lot of efficiency to get there. The other metric of course is average account size, but the more efficiency you can create, the lower your average accounts can be. In full transparency, our first business plan assumed an average client balance of $100K. Over time we have far surpassed that. And I think it's only going up from here as we've realized this platform can be used to serve not only clients below a million, but in the $1 to $3 million range. Our average balance is only going up and we're only getting more efficient. Alex: What recommendations do you have for others thinking about how to build out their tech stack? Any resources you’d recommend? Brad: I typically recommend that before people look at available technology solutions, that they start with a whiteboard and draw what they need the technology to do. Then find the tools that fill that need. As far as resources, I’ve scooped up tons of information from #fintwit on Twitter. I think in this new economy that you don’t have to be a developer. For instance, you can build a website yourself much more cheaply than you could 10 years ago. And with subscription-based tech, you can find solutions that allow you to connect everything together yourself. The reality is the operating cost of running a business like ours over the last decade has declined substantially. But not everyone knows or realizes that yet. Alex: What would you tell advisors who might be skeptical of using a platform like a Betterment or someone else's? I think there's always skepticism around whether an algorithm can perform certain activities such as trading, rebalancing, and asset location. However, the contributions of an automated platform with impressive technology and execution can really shine during a situation like COVID, which came upon us so fast, but was met with industry high records of near-daily rebalancing of client accounts on certain high volatility days. Most human trading teams probably couldn't keep up with that pace. The other concern that advisors may have would be working with a lesser-known custodian. In my mind, custodians are more of a commodity at this point. It becomes a non-issue for most people once you educate them on what a custodian does, what they don't do, and what it really means to be somewhere else, while also articulating the advantages that they can give you. Finally, the Betterment UX provides people a clear, visual representation of their whole financial picture in a way that I don't think anyone's ever gotten with other online platforms or traditional custodians. Alex: Any parting comments? Brad: The one message I would like to tell everyone is don't just think about Betterment as a way to serve one segment of your existing high net worth business. Go out and build a business to serve the broader population because the market opportunity there is huge, there's no competition, and millions of people need financial advice. We hope that other advisors can learn from our experience in their consideration to utilize automated platforms and other tools. -

![]()

Betterment for Advisors Case Study Q&A: How Ritholtz reaches a new client segment

Betterment for Advisors Case Study Q&A: How Ritholtz reaches a new client segment Matt Lohrius oversees the Liftoff platform at Ritholtz Wealth Management, which began leveraging Betterment’s platform more recently. Ritholtz is located in New York City and manages more than $2.7 billion in assets. Non-paid client of Betterment. Views may not be representative, see more reviews at the App Store and Google Play Store. Dan: Tell us about how the sort of robo-advisor aspect of things works within Ritholtz Liftoff. How do you guys organize it and think about it? Matt: As you probably know, our core business was focused on high net worth households, people that were staring down retirement or leading up to it. And we put out a lot of content—whether it's blogs or The Compound (our YouTube channel)—so a lot of people are following us and telling us they’d like to become clients. But many of them didn’t fit our traditional high net worth, pre-retirement customer profile. But clearly there was a demand, and we wanted to help these people. So that's why we created Liftoff, which we’ve continued to improve over the years. But it really blossomed once we started working with automated platforms like Betterment. There’s no minimum, so it’s great for people in their twenties or thirties who are maybe just starting to invest. Dan: Tell us a little bit more about Liftoff’s ideal client profile. Matt: There are a couple of different types. One would be someone who's on the younger side and who is in the accumulation stage base. They may not yet be married or have a family, but they’re starting to make money and they want to save in a smart way. This type of investor also wants access to an advisor for questions that do arise: around what they should be doing differently when they do get married or start having kids. I also love talking to people who have just graduated college, because they’re such enthusiastic followers of ours. We’re happy to accommodate them. Dan: This is obviously a big potential for growth. How do you think about growing Liftoff? Matt: I think we want to grow it as big as we possibly can and take it as far as we can. And that's kind of my mindset: I get on the phone with everyone who wants to chat. Hopefully we do get to the point where we need to bring more of me to oversee twice or three times as many Liftoff clients as we have right now. Dan: What have been the biggest hurdles to growth so far? Matt: One hurdle is that there's always going to be people out there that would rather just do it themselves and that's fine. We totally understand that. But there are still plenty of other people out there who don't even know where to start. And so we're looking to reach that group of people. Dan: Do you find that there is a catalyst that brings the self-directed types to you? Matt: Yeah, it could be a year like this one that we're in right now where people who have been investing on their own for a while reach out because of all the uncertainty. They are looking to get a little more advice. Dan: Talk a bit about the culture within Ritholtz to new technologies. Matt: We're all about it. Outside of the Liftoff channel, Ritholtz is looking at technology to onboard clients more quickly and smoothly. We know it’s possible—with Betterment and Liftoff, you can open an account like that. So we want to be able to expand that kind of capability throughout our entire firm. And that really just involves us looking at all the technology we currently have to streamline the client experience. Dan: Can you talk a little bit about the difference that an automated platform like Betterment makes in your day? Matt: For Liftoff, it’s just huge from a technology standpoint: opening accounts, transferring money from other custodians, depositing money, linking a bank account. Everything is so easy and intuitive for the client. And that saves us a lot of time: we’re not having to help a client with the logistics of opening an account and can spend our time with them focusing on advice. That's where platforms like Betterment really excel, with the operational efficiencies. I think a lot of advisors hear “robo-advisor” and sometimes get a little turned off, but who doesn't want operational efficiency? And that’s on both sides of the equation to clients and advisors. Dan: What if you go back, what initially sparked the interest in convincing you to start using a robo-advisor as a partner? Matt: It’s kind of just set it and forget it. It's easy. You have a durable, long-term portfolio. You're going to invest in it just to keep saving. That's the work that you need to do, is constantly save. And outside of that, you don't need to do a whole lot. It's helpful for a lot of people. And when we do have a client ask “Can I do my own thing?"—because there’s often that temptation—we tell them “No, you can't.” That's the whole purpose and benefit of this. You can go somewhere else and do that. But if you want a concrete long-term plan, this is where you're going to get it, and it's very likely to work. Dan: What would you tell advisors who are skeptical about using a robo-advisor? How would you help them to understand how well it's worked for you and your clients? Matt: People who are skeptical need to realize that this is a hybrid platform. Yes, the portfolios and operations are automated, but you have access to an entire firm. Because if you have access to me, you have access to all the resources that I have access to. And that can be powerful. Dan: Last question. Does using an automated platform like Betterment mean that you, as a CFP®, as an advisor, get to spend more time on bigger issue questions like planning? Matt: Yes, one hundred percent. That is the whole reason Liftoff switched to Betterment. With the custodians we had been using previously, there were a lot more operational emergencies that needed our time and attention. But with a platform like Betterment, all of that is taken care of so that we at Liftoff can focus solely on providing quality advice. That's all we want to do here. Automation (through Betterment’s platform) is allowing us to do that now, which is why I'm confident that Liftoff will continue to grow. Ritholtz Wealth Management is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where Ritholtz Wealth Management and its representatives are properly licensed or exempt from licensure. This website is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by Ritholtz Wealth Management unless a client service agreement is in place. -

![]()

Q&A with Paul Sydlansky of Lake Road Advisors

Q&A with Paul Sydlansky of Lake Road Advisors A conversation about going independent and scaling your business using the Betterment for Advisors platform. Paul Sydlansky is the founder of Lake Road Advisors, an independent, fee-only financial planning firm. He has worked in the financial services industry for over 20 years. Prior to founding his firm, Paul worked as a relationship manager for another RIA. He also spent 13 years at Morgan Stanley in New York where he was a senior level manager in the institutional equities department. Paul is a Certified Financial PlannerTM, a member of NAPFA and a member of the XY Planning Network. Non-paid client of Betterment. Views may not be representative, see more reviews at the App Store and Google Play Store. Q: Tell us a little bit about your practice and the factors that you think have contributed to your success in growing your RIA. Lake Road Advisors is an independent, fee-only financial planning firm. We specialize in working with mid-career professionals who have young families and that's been developing over time as our niche. Right now we have about 100 client relationships and manage roughly $60 million in assets. We have offices in upstate New York and in Long Island. We launched the firm in 2016. Before that, I was at a RIA where my views, goals, and values were not in line with the firm owners. For me, launching the firm was about sticking to my views – simplifying things for people, making things easy, and really focusing on what adds value to my clients. And for the niche that I work with, it's having somebody who is an accountability partner – somebody to bounce ideas off of, who can worry about all these things that generally folks don't have time to do, but they realize are super important. Focusing on those clients’ needs and making their lives easier has really led to our growth. Q: What were the biggest hurdles that you encountered when you were initially growing your practice, and how did you navigate those? Starting from scratch. I had a non-compete at the firm I left in 2016 so I had to start with nothing. Planning out my runway was difficult. I think for anybody who's thinking about starting their own firm, it's always going to be longer than you assume – if you're budgeting, I recommend you assume the worst and then add two or three times that in terms of how much you need. That was very difficult for me, starting from a position where really all you had to focus on for the first year or two was growth and making sure that I was developing enough of a client base to make the business viable. I was lucky that we had some good growth to start with and now my challenges are all different. But that was the biggest one – making sure that financially I had enough runway, I could still live the life I wanted and support my family while I was doing it, and making sure I was doing things the right way. Q: What role has Betterment for Advisors played in your growth over the last few years? When I was at Morgan Stanley, I was in private wealth management for a couple of years, but I spent the majority of my time in prime brokerage working with hedge funds. So I came into the financial planning business with a kind of skewed view of investments. I'll be honest, I believe in hedge funds and alpha creation and the ability to outperform. And as I've evolved as an advisor, I've really done a 180 and realized that for the majority of people, trying to chase alpha is not really going to change their life. What's going to change their life is focusing on blocking and tackling their cash flow, their spending habits, their balance sheet, not making silly decisions, creating good habits. Of course, we'd all like extra return. But I think the pursuit of that is going to be fruitless for most, and for the majority of people, having a simple, low cost, diversified portfolio just makes sense. So the firm I was at was an active manager and I saw firsthand what a disaster that was, to try to manage 800 individual portfolios and do things like tax-loss harvesting or rebalancing. It was just a nightmare and they spent a ton of time doing it. And in my opinion, it didn't really add much value to the end user because the manager was actually underperforming a lot. So for me, Betterment was number one given that the platform is easy to explain to my clients. Most of my clients obviously understand investing, but they don't want to spend too much time on it. Betterment allows me to do that. It's straightforward. They have one page in the app where they can click to see their performance and really quickly understand. It keeps things super simple. I don't spend any time on things like rebalancing, I don't spend any time on things like tax loss harvesting. It's all automated. And I know that frees me up to do things that actually will add value to clients. Q: Is all of your AUM at Betterment or do you use other custodians as well? Yes, so the majority is – I have a portion of it that is with Vestwell on their 401(k) platform. I have no other partners – it's all Betterment for my individual clients and then for my five clients who are on the 401(k) platform as well, that's the other system I'm using. Q: How does Lake Road position Betterment for Advisors to its clients? I've obviously had this conversation tons with different advisors. Everybody seems to be hesitant to partner with Betterment, saying – well, aren't they your competitor? Absolutely not. Because the way I view it is Betterment is a partner and a technology platform. So that's how I position it. First and foremost I say I'm a registered investment advisor. I am not a bank, I am not a broker-dealer. I've partnered with another firm who can allow me to leverage a system that really buys in perfectly to how I believe investing should be done for almost everybody. So for me, I position Betterment as a partner, as a technology solution, and I don't see it as competition. Q: How do you price your offering and how do you communicate your firm's pricing to your clients? Great question. What I do is tell the client one all-in price because as everybody knows, pricing can be confusing, and I try to just be as straightforward as possible. For anybody under a million in AUM, it's 1.25%. And again, usually it's a half a million minimum of assets. And the way I tell that to clients is that ultimately, I have a set amount that I'm trying to make for the firm, and a percentage does go to me, and a percentage goes to Betterment. My fee is for the planning work and obviously helping with the investments. And then part of that fee goes to Betterment for the technology and for all the tools that they're providing us to use. But I like to present it as an all in fee. And in addition, I have breakpoints. So if a client hits a million, that all-in fee drops to 1.1%, and then so on. I also have another offering where I have clients who have no investment management. It's just straight planning. And for those clients, it's a flat $5,000 a year. They are not on the Betterment platform, but it's another way for me to work with young families or folks who have assets tied up in their business and don't have the assets to manage right now at this point in their life. I'm up front with clients and say, “I only have so many seats on my bus.” I have one other gentleman who started working with me late last year. And so now that we have 75 relationships, ultimately I'm looking to try to make $5,000 minimum on each one of those seats because I know the amount of planning work we do. I know how many touch points we have, how many meetings, how many calls, how many zooms, how many visits. And so for me, that's kind of the minimum where I want to be with the amount of service that we're going to provide, the relationships that we're looking for to grow the business. Q: Are you typically using Betterment’s investment portfolio? Are you using different portfolio strategies for clients? Right now I'm using Betterment strategies for the majority of clients. I thought about creating my own portfolios but for the amount of time it would take me to research and keep on top of it, it just didn't seem like I was adding any value there. In addition to the Betterment portfolios, I've used the BlackRock portfolio, one of the income generating portfolios for a client where it was appropriate. Q: Aside from Betterment for Advisors, what else is in your tech stack? I use MoneyGuidePro on the planning side and my CRM is Wealthbox. I've been using Riskalyze and I've been really happy with them in terms of storing and having an IPS, and it's a great conversation starter and just a way to explain risk a little bit better to clients. I use Calendly. I think most people probably use something, but Calendly has been a huge time saver for me, for my business. Q: What are your client acquisition strategies? I've been pretty lucky in that when I look at the tracking of where my clients have come from, they've been pretty evenly split from a lot of different sources. The first has been friends and family. Another one is current client referrals. And a third one has been networks or traditional centers of influence like lawyers and accountants. In terms of marketing, I write a blog. I have over 100 blog posts now and while it was tough to do, it's a really good marketing tool. I answer questions on it that I hear all the time from clients and prospects. So if a client or a prospect reaches out I can tell them I just wrote a blog post about that. I also started to do some videos. Creating awareness and really connecting to your niche or your target market is huge. I went through the exercise of figuring out exactly who I want to work with and with everything I do from a marketing perspective, I try to speak to that person. That’s really been a driver of growth. Q: What would you tell advisors who might be skeptical of using a platform like Betterment or something similar? You need to think about your practice and where you add value to your clients. I do believe that there are folks out there for whom active management can make sense in some instances. But I think you really need to figure out how you're positioning your firm for the future – is it the planning you're going to focus on or is it the investment management? Where are you going to add value? What's going to differentiate you from other advisors? If you think that you're going to be focusing on planning and the relationship and accountability and all that type of stuff, choose something that automates other work for you. Because you going in and clicking a button to rebalance does not add any value and it just takes away from other things you could be doing. Q: How do you answer questions from clients that want to have positions that aren't part of the Betterment models, such as single stocks? What do you tend to say to them? Yeah, that's a great question. So I think that goes to fit upfront. I have a conversation upfront about my investment philosophy and how I don't really believe in holding individual positions. Ultimately, we do work with some executives and they have restricted stock and individual positions and options and you can't get around that. So what I tell people is if you're going to have individual stocks, by all means have a Fidelity account. Have a Charles Schwab account. Have a Vanguard account where you can do that as long as you want to trade it on your own and you're doing it outside of what you’re doing with me. Q: As an advisor who's also a business owner, how do you keep up with compliance as you grow your business? When I launched my firm, I launched with XY Planning. They helped me get up and running, but I outgrew it and needed a little bit more help. Since I'm in New York, I had to be SEC registered. I work with an individual who basically opened up a compliance firm that helps folks like us – the smaller size advisor. So I have an individual lawyer who helps me with the compliance. Because I'm still on the XYPN platform, I also use something called Smart RIA that's like a CRM for all of your tasks and all the things you have to do for compliance. And the other thing is, my business is super simple because of the nature of the investing. For anybody who's done the ADV, a lot of the questions are around investing and advice and things like that. My investments are so simple and so vanilla that I think because of the reduced complexity, it makes compliance a little bit easier. Q: Do you have any advice on how to coordinate your IPS with the Betterment portfolios? As part of my onboarding process, I make people go through the risk process. I use Riskalyze which connects with Wealthbox. So I check a box, and once a risk score is in Riskalyze it flows to Wealthbox, and it populates a field for me so I can see the score when I pull up the client. And then on top of that, when we start building out their plan in MoneyGuidePro, we have the ability to make sure that that score translates to Money Guide Pro. It’s not perfect right now, but it goes between those different systems. Q: The transition to remote work has been a popular topic. How have you adapted to that? Is there anything new or different that you're doing to connect with clients and prospects? No, remote work has honestly been completely seamless. From a system standpoint, I worked from a home office already. From a marketing perspective, it's really made me realize how important your online presence is. Everybody knows your website and blog and all that is important, but I started doing video too because I feel like it's a better way to connect with people. I've been using something called Loom, and I also took a class about how to do videos and best practices. Before I meet a prospect, if somebody reaches out online, I will send them a quick 20-30 second Loom video saying: Hi, I'm Paul. Thank you so much. I'm really excited to meet you, if you could just prepare this and that for our meeting, and so on. I've been told it has been really positive because people feel like they know you before they talk to you. Now I'm trying to incorporate it into my client service process too. So every once in a while if I have a follow up task, I can send someone a quick video and say, hey, it's Paul, we took care of that Roth conversion, you're all good to go, have a great day. Little things like that, I think those are going to be more important going forward. Seeing people on Zoom can be tiring, but getting a quick short video from somebody, a friend or somebody who's helping me with something, it's really nice versus an email. So I do think for me and my firm, it's going to be more focused on video, leveraging that and using that as a way to connect. Q: One last closing question: What advice would you give to new advisors who are just starting out? Aside from making sure that you have enough cash to weather the storm of the ups and downs, I think the other thing is making sure if you have a spouse or partner, whoever's going to be there with you, that they're bought in. Aside from the financial stress of starting something new, don't discount the emotional ups and downs you go through on a day to day basis. Having somebody who's supportive and who can be there in the good and the bad is very important. Your emotions go all over the place and it's still that way. As an owner, I don't know if it will ever change. I think it's leveled out a little bit but I still want to grow. If you would have told me when I started where I’m at now, I'd probably be really happy. But now I want to get to $100mm or $250mm. I'm thinking about my firm and what people I need to help me get there. So I just think having support at home from that person and making sure they're bought in is huge. Because if you don't have that, it's probably going to be difficult to do it.

Product Guides

-

![]()

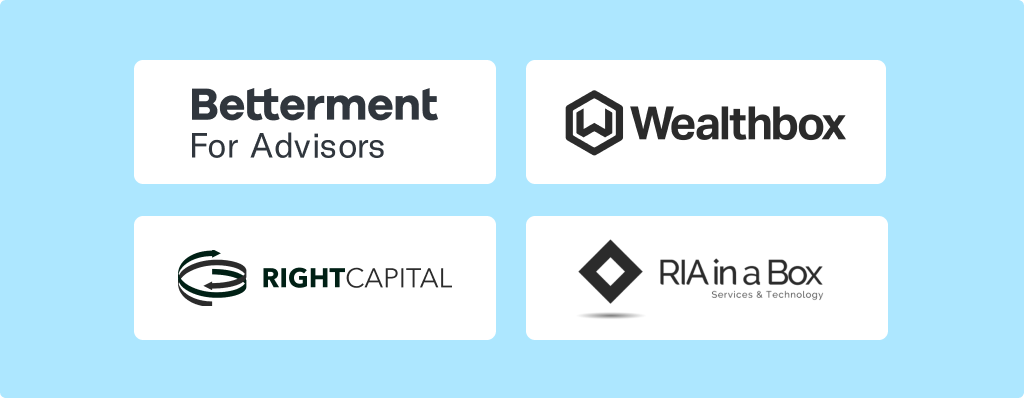

Introducing the RIA Tech Suite

Introducing the RIA Tech Suite The RIA Tech Suite brings together complementary technology platforms to help automate critical back-office tasks for advisors. The RIA Tech Suite brings together complementary technology platforms to help automate critical back-office tasks for advisors. Along with RIA in a Box®, RightCapital, and Wealthbox, Betterment for Advisors is excited to introduce the RIA Tech Suite: a set of services and tools that advisors can use to help automate and streamline back-office tasks. Why should firms utilize the RIA Tech Suite? Together, these intuitive and complementary tech tools can streamline everyday practice management, giving you more time to acquire new business and to provide a better experience for your current clients. Additionally, the RIA Tech Suite includes discounted pricing for firms that adopt two or more of the services—a discount that could save the average RIA firm up to $3,200 in their first year.1 Here are the tools available on the RIA Tech Suite: Betterment for Advisors - A leading digital-first wealth management platform that leverages smart-tax technology. RIA in a Box® - Compliance, cybersecurity, and operational software for investment advisors. RightCapital - Wealth planning software that makes planning easier and more powerful for advisors and their clients. Wealthbox - A leading CRM software application that helps advisors manage their clients and collaborate with their team. The RIA Tech Suite can foster growth for tech-centric firms that are focused on efficient client service and expanding their books of business. “Our goal at Betterment for Advisors is to empower advisors to grow their businesses and build deeper client relationships,” writes Jon Mauney, General Manager of Betterment for Advisors. “The four companies that are part of the RIA Tech Suite all share this objective with a common approach to their services: providing beautifully designed, easy-to-use, and powerful tools for advisors and their clients.” The RIA Tech Suite is now available to all registered investment advisors. You can learn more and sign up for this offering by visiting https://riatechsuite.com. Betterment for Advisors is a member of the coalition known as RIA Tech Suite alongside three other platforms: RIA in a Box, RightCapital, and Wealthbox. The four companies are offering advisors who become new clients of two or more members of RIA Tech Suite, discounts on services provided by such participating companies. Betterment and aforementioned firms are not under common ownership or otherwise related entities, and no compensation has been exchanged between the members of RIA Tech Suite for the purposes of entering into this coalition. Terms subject to change. This offering is for investment professionals only and is not intended for use by private investors. ¹ 3200 USD is an estimate of the maximum amount saved on the annual cost for combined subscription fees across all four services noted in this article. Calculation assumes the average of weighted monthly rates offered across all four services plus their onboarding fees, which are subject to change at each service providers’ discretion, and then applies a 15% discount from each. The discount rate of 15% per company is activated upon engagement of a minimum of two companies. Actual dollar amount saved may vary; Betterment makes no guarantee of the specific dollar amount your firm could save. -

![]()

FAQ: Agreement Automation Process

FAQ: Agreement Automation Process The Betterment for Advisors Client Agreement Automation function will make onboarding your new clients fast, easy, and completely paperless. Will my firm need to update our ADV and/or Customer Agreement to reflect the incorporation of Betterment for Advisors into my practice? Yes, you will need to update your Form ADV Part 2A and most likely your Customer Agreement to reflect the incorporation of Betterment for Advisors into your practice, including (among other things) how your firm uses Betterment’s sub-advisory and brokerage services, and Betterment’s fees. Since each situation is unique, please consult with your attorney or compliance officer. Can Betterment for Advisors automate the signing of my agreement with my client? Yes, you can provide PDF versions of your client agreement, Form ADV Part 2, and privacy policy to include as part of the electronic signup process a client undergoes with Betterment. We also provide reporting in your dashboard about which versions your clients have agreed to, and when. You can read more about our agreement automation feature, including legal disclosures, here. What relationship does the client have with Betterment? Betterment acts as the sub-advisor to your client. You still remain the primary advisor to your client. When your client goes through the new account opening process, they will sign an agreement with Betterment directly as the sub-advisor, and, if you wish, an agreement with your firm directly as the primary advisor. Describe the process your product uses to convert information provided by the client into a risk profile in the interview process. The platform automatically recommends investment goals and associated recommended allocations for each such goal for new accounts established on the platform using the client’s age, information provided by the client during account creation regarding a particular financial goal, and the type of legal account. Am I able to see an archive of electronically executed client agreements? If so, what does this look like? If you enable the agreement automation feature to deliver a paperless account opening process for your clients, an archive of the date/time stamp and the version of the agreement that each client electronically signed is housed on the “Agreements” tab of the advisor dashboard. To learn more about our agreement automation feature, please see here. -

![]()

Questions about Using Dimensional Funds through Betterment for Advisors

Questions about Using Dimensional Funds through Betterment for Advisors Advisors using Dimensional Funds through Betterment can create their own models from scratch or select from a range of pre-built models What is the process for becoming approved for access to Dimensional Funds on the Betterment for Advisors platform? Generally, you will go through an introductory and educational meeting with Dimensional Fund Advisors, after which you should be approved to access Dimensional Funds on our platform. This process can be accomplished in as few as 2 to 3 days. Please email connect@bettermentforadvisors.com to kick-off the approval process. If I am an advisor with access to Dimensional Funds, can I also access them on Betterment for Advisors? Yes, if you are already an advisor with access to Dimensional Funds, you will also be able to access them on the Betterment for Advisors platform. Please contact us at support@bettermentforadvisors.com and we will enable access upon verification from Dimensional Funds. If I already use Betterment for Advisors and have been approved by Dimensional, how long will it take me to get access to create and use Dimensional portfolios once I've made the request? Once you’ve notified us via a message to support, we’ll update your Dimensional Funds status in the Betterment for Advisors platform within 2-3 business days. You’ll receive a confirmation email from us at that time. If I'm new to Betterment for Advisors, how long will it take me to get access to Dimensional Funds once I've completed the process? We typically review new firms on the platform within 5 business days. Please notify us during this time that you are approved to sell Dimensional Funds by sending a message to support@bettermentforadvisors.com. This will allow us to provide access to the Betterment for Advisors platform + Dimensional Funds as soon as your firm’s application is approved. Will there be model portfolio templates available for me to use? We have several templates available for administrators to use as a starting point. Each Dimensional Funds template portfolio corresponds to a specific allocation between equities and bonds and is intended to be broadly diversified. You can use these templates as a starting point. The colleague(s) who have administrator access to Betterment for Advisors will be able to create custom model portfolios using Dimensional Funds. This allows for adjustment of the funds included in the portfolio and their weights. How do I create my own portfolio once approved? Once your firm is approved for access to Dimensional Funds via Betterment for Advisors, your firm's admin person will be able to create model portfolios with Dimensional Funds. It’s easy to create and brand your own custom portfolios from scratch. Firm admins can create client portfolios directly from their Advisor Dashboard through 3 easy steps: Select the “Portfolios” tab on the left Choose the tab labeled “Dimensional Portfolios” Select “Create Portfolio” If additional members of your team need administrative access to the platform, simply have your firm’s primary contact notify us at support@bettermentforadvisors.com. Contact us if you want to become approved with Dimensional Fund Advisors or learn more about Dimensional Funds on the Betterment platform. If you click the link above, Betterment may share your firm name with Dimensional in order to determine firm eligibility to use Dimensional Funds.

Explore key topics for RIAs

Not a Betterment advisor yet?

Get started with Betterment for Advisors.

Explore our trainings for new advisors

-

![]()

Training Video: Sync External Accounts

Watch our product training video on how to assist your clients in connecting external accounts to ...

Training Video: Sync External Accounts Watch our product training video on how to assist your clients in connecting external accounts to the Betterment experience. -

![]()

Training Video: Link a Bank Account

Watch our product training video on how to connect a funding account to help your clients transfer ...

Training Video: Link a Bank Account Watch our product training video on how to connect a funding account to help your clients transfer cash into Betterment.